Does PPI move Treasury yields?

Most similar past releases: August 2013, December 2015, December 2019

Reported figure: U.S. government release. Market move: change from the prior close, Federal Reserve Board data via FRED. "Normal day" is that calendar year's average daily move. Browse every release.

The Producer Price Index (PPI) measures inflation one step up the supply chain from the more famous CPI — prices received by producers rather than paid by consumers. It typically lands within a day or two of CPI, and traders watch it partly for its own sake and partly as a tell for the next consumer-inflation reading. The question here: when PPI prints, does the bond market actually move — and where on the curve?

We measured the reaction across 36 PPI releases, focusing on the rate-sensitive 2-year Treasury, and compared it against a baseline of ordinary days.

Verdict

- Direction (release day): Not Significant

- Volatility (release day): Significant

- Volatility (5 days): Not Significant

PPI — the wholesale-inflation report — moves the rate-sensitive 2-year Treasury about 1.5× a normal day (p=0.03), but you cannot predict the direction. The 10-year reacts less.

Bottom line: PPI nudges short-term rate expectations — a real but moderate move, with no reliable direction.

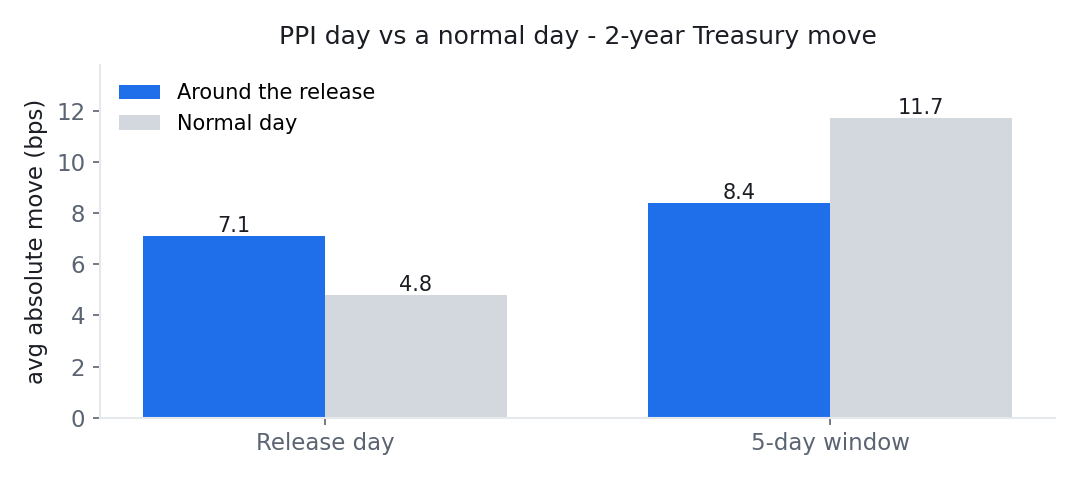

Average absolute 2-year yield move around PPI releases versus normal days (N=36). Chart: Macro or Noise, from Federal Reserve Board data via FRED (public domain).

What the numbers say

On release day, the 2-year yield moved about 7.1 basis points versus 4.8 on a normal day — roughly 1.48× a normal day, and statistically significant (p=0.03). So PPI is a genuine mover, but a moderate one, and its effect is concentrated at the front of the curve.

Direction is a coin flip: the average signed move was about −2.3 basis points with a p-value of 0.14 — not distinguishable from zero. As with every inflation release we test, hot and cool surprises offset, and you cannot position for the direction using the release itself.

The effect is also short-lived. Over a five-day window the front-end move is actually smaller than a normal week (about 0.72× baseline) — there is no lasting drift, just a release-day flicker.

Why the front end, and why less at the 10-year

PPI matters to the bond market mainly as information about near-term inflation and therefore near-term Fed policy — and near-term policy expectations are priced at the short end of the curve. That is why the 2-year reacts most. The 10-year, which reflects longer-run growth and inflation expectations, moves less: about 1.33× a normal day, which is only borderline significant. You can see PPI's full footprint across every maturity on our Treasury curve map.

What this means in practice

- A second-tier inflation mover, felt at the front end. PPI reliably adds some movement to the 2-year, but it is smaller than the jobs report or CPI, and mostly bypasses the long end.

- Direction is not tradable from the release. The signed reaction is indistinguishable from zero.

- It is a release-day event. No lasting drift over the following week.

None of this is advice — it is a description of what 36 releases actually did, and results can change with a different sample, period, or definition.

Key findings, generated from the data

- Across 335 releases, the 2Y moved an average of 3.79 bps on release day (absolute).

- The largest single reaction was -27.0 bps on 2023-03-15 (February 2023 data).

- Splitting by our trend-based surprise shows no reliable directional pattern: pooled p=0.11, and by era — 2000-2012: -0.23 (p=0.80); 2013-2019: +1.79 (p=0.01); 2020-2026: +1.38 (p=0.42). Note the sign is not even stable across periods.

- Because our surprise is a trend proxy rather than a market consensus, and because these splits are sensitive to the period chosen, treat all of the above as patterns observed in this sample rather than as established effects.

- Surprise size does not clearly scale the reaction: the largest third of surprises averaged 3.43 versus 2.64 for the smallest third (p=0.26).

Generated automatically from our event database by a rule-based script (no language model). "Surprise" is model-based — the reading minus the average of the previous three — and is not a market consensus forecast. See every release in the database.

The data

| Dimension | Horizon | Value | Baseline | Test stat | p-value | Verdict |

|---|---|---|---|---|---|---|

| Direction | release day | -2.3 bps | 0.0 bps | -1.53 | 0.135 | Not Significant |

| Volatility | release day | 7.1 bps | 4.8 bps | 1.48 | 0.029 | Significant on its own |

| Volatility | 5 days | 8.4 bps | 11.7 bps | 0.72 | 0.934 | Not Significant |

(Values are for the 2-year Treasury, the maturity where PPI's effect is largest.)

Methodology

- Events (N): 36 PPI releases.

- Window: 2023-01-18 → 2025-11-25.

- Measurement: change in the 2-year yield from the prior close to the close at the end of the holding window (look-ahead protected).

- Baseline: the unconditional distribution of same-length moves across all trading days.

- Tests: one-sample t-test of the signed move against zero (direction), and a bootstrap of the absolute move against the baseline (size).

Caveats

- The effect is on the 2-year (front end); the 10-year move is weaker but also clears its own bar (×1.33, p=0.04).

- The event study above does not condition on surprise: it measures the reaction to the release itself. The "Key findings" block does add a split by our own trend-based proxy, which is not a market consensus forecast — consensus data is proprietary and outside our public-domain sources.

- Historical statistics for informational purposes only, not financial advice. Results may vary with sample, period, and baseline definition.

Related tests

- Does CPI move the 10-year Treasury yield? — the consumer-inflation counterpart.

- Do jobs reports (NFP) move Treasury yields? — the biggest scheduled mover.

- Which U.S. data releases move the Treasury curve? — PPI in context across maturities.

Source

- 2-Year Treasury Constant Maturity, Federal Reserve Board via FRED (Tier A, U.S. public domain) — DGS2.

- PPI release dates, U.S. Bureau of Labor Statistics — Producer Price Index.